|

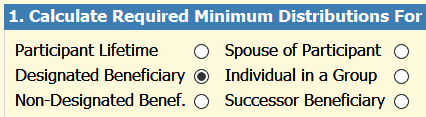

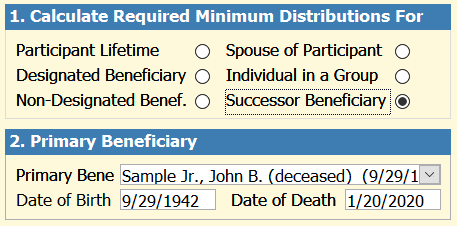

The SECURE Act of 2019 dramatically altered the rules for Required Minimum Distributions (RMDs) for designated beneficiaries. The distribution of an RMD to a designated beneficiary or a successor beneficiary now depends upon the date of death of the participant. If the participant died before 2020, leaving the account to a designated beneficiary, the 2001 rules apply. The designated beneficiary may continue receiving RMDs under the old “stretch IRA” provisions.  On the other hand, if the participant died after 2019, the designated beneficiary must follow a new 10-Year Rule wherein account custodians must distribute the total amount of the retirement account within ten years. We added another option Step 1 to accommodate the 10-Year Rule, specifically, the “Successor Beneficiary” option for participants dying after 2019.  If the successor beneficiary dies during the 10-Year Rule period, the next successor beneficiary falls under the original successor beneficiary’s 10-Year Rule (based on the date of death of the participant). Effectively, there is no “10-Year Rule reset.”

The marginal tax rates come into play as distributions are made. ProTracker Software’s ProTracker Advantage® client relationship management (CRM) system documents the distribution decisions to assist the advisor in remembering the client's parameters. Learn more information about calculating RMDs and documenting them here.

0 Comments

Leave a Reply. |

|

RSS Feed

RSS Feed

|

ProTracker RMD Calculator Assistant was developed to take the headache out of calculating and tracking RMDs, which has become even more odious with the new SECURE Act. Our experience as advisors gives us a unique understanding of your needs, and our goal is to make your business more efficient.

To learn more about ProTracker Advantage® (CRM) for your firm, fill out our CRM evaluation form. We respond to all inquiries. |